Creating Cash Value in Your Medical Device Company

Presented by Deborah Douglas, Managing Director, Douglas Group at the 10x Medical Device Conference – San Diego 2019

Reading Time: 14 minutesDeborah Douglas:

Hi. Douglas Group is a firm which sells companies. That’s all we do. We represent sellers, a hundred percent.

The objective of sellers in the medical device space is a little bit special, relative to other sellers in the world. I would say medical device owners want one plus one is 10. Other people want one plus one is three, five maybe. But the medical device owners really want a much more aggressive stance.

Most of the medical device owners who come to us come to us a little ahead of time, before their company is really ripe, before it’s really ready for sale. But some not.

Let me get a little feel for this audience, if I could. How many people in this room own all or part of a medical device company of your own? Okay. How many people here work for a medical device company? That’s a bigger part of the population. The other thing I hear a lot of as I talk to people are service providers to medical device companies. How many people own a service provider? Okay. And how many people work for a service provider? Okay, so it looks like that’s maybe half of this group, something like that.

We sell companies. We’ve been doing it for a little over 25 years. We’ve sold 130 companies. Most of those weren’t medical device companies. For the first 10 or 15 years, we focused pretty much entirely on manufacturers, plastic manufacturers, and metal manufacturers. Only in recent years have we really gotten excited about this segment. And it really is an interesting segment.

I’m a big believer in what we do. I think it’s really a good thing. I grew up with a guy who came from Communist Russia, way back when. This’ll date me! And he had an expression. He said, “Free enterprise is shameless exploitation for the common good.” I like that! I’ve always believed in that incentive being there for business people making a really big difference in the marketplace. My eldest daughter was home from Cornell recently with a bunch of friends, and they were all talking, and I couldn’t help myself. I kept throwing them little comments. And, finally, my daughter stopped the whole conversation, and she said, “You have to understand my mom! She thinks there’s some kind of healthy selfishness that’s really good for the world!” I do! I think that’s true.

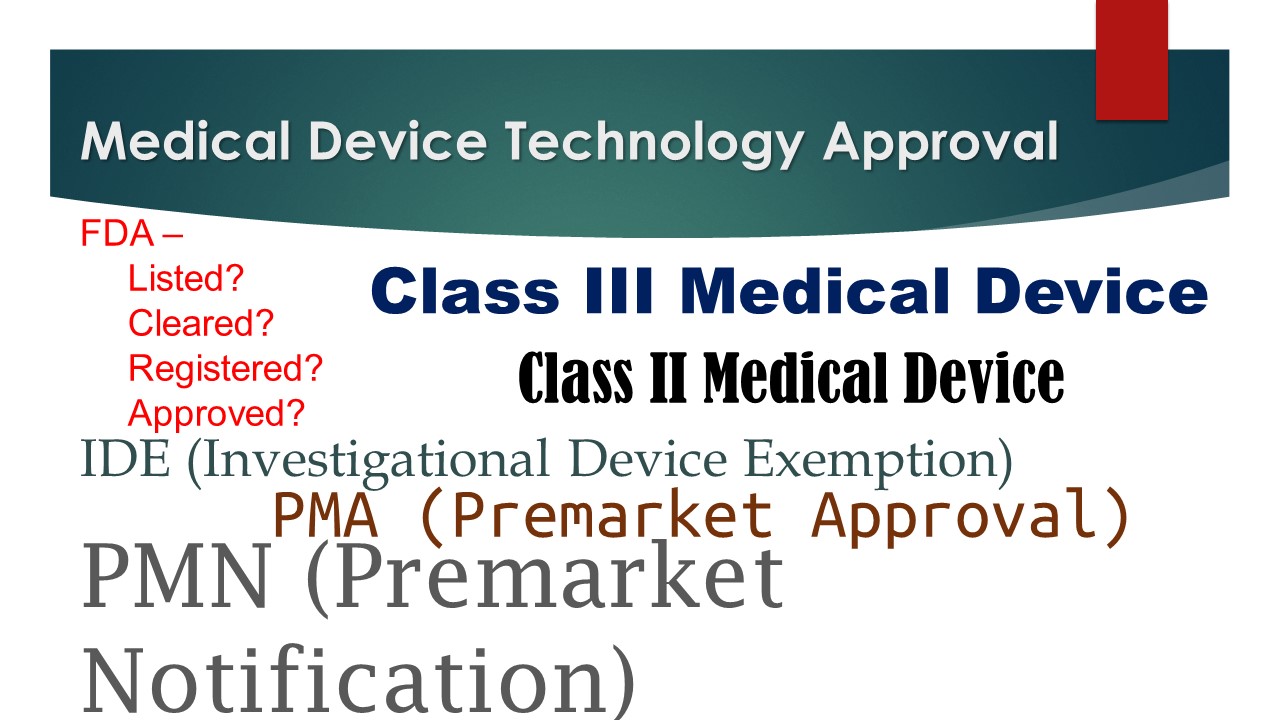

Medical Device Technology Approval

When you talk about the medical device space, too many of the people that come to us come a little bit too early. They come before their technical approval is quite in place, and that’s really hard to do. You really can’t make it work that way.

The FDA currently regulates 190,000 medical devices in the U.S. And, of those devices, they’re made by some 18,000 different companies in the U.S. It’s a big group. It’s a big population. And businesses have to deal with really complex rules in this space.

How many people here get involved with helping owners get technical approval? A pretty good number! It’s a pretty good number of the mix. I think it’s very critical, and it’s really important to the process, and we try to wait until we get there.

Salability Foundation

Some owners come to us before they’re quite ready. That’s fine. We can deal with that sometimes, but we can’t deal with it too far in advance. Or, it’s just not going to work. It’s going to hurt value so much.

Or, the other thing that happens to business owners is they come before they’ve gotten a final approval. And then, the investors who come in behind them, they don’t want to buy the company. They want to reimburse you for part of your cost and get a majority ownership for doing that. And that’s not where most business owners want to be. It doesn’t work too well.

When we talk about the salability foundation, we really talk about trying to wait until technical approvals are in place. Some initial sales have happened. That does not have to be huge. We’ve sold a lot of companies that literally multiplied by ten within a couple of years of acquisition.

We have to have the technical approvals in place, and we have to have the initial sales at least well-begun. We sold a company not too long ago. This was about three years ago. And, the company was smaller than our average. Most of our companies are $10 million to $100 million in sales. This one was about $7 million, so it was youngish, relatively. Had great profitability, and, frankly, we had to create a lot of competition to get the pricing right for that company. We ended up with about 20 offers, less than $10 million. It was frustrating. It was hard to do. But, we had two offers north of $30 million, so we closed it for $32 million, and everybody was happy. It worked out well. You don’t always know that’s going to happen.

You have to be able to show some production beginnings, not very far along, but you at least have to have good estimates of what production costs are going to be. We have a lot of clients we’ve dealt with in the very early phases where, in their first production runs, costs were 70% of sales. That’s tough, and that’s hard to deal with. But, if you can show that, as soon as that sales volume ratchets up, those costs are going to go way down, it helps a lot. We see a lot of companies start at 70% of sales and end at 20%, or 25%. And, buyers can see that. Buyers are aware that might happen.

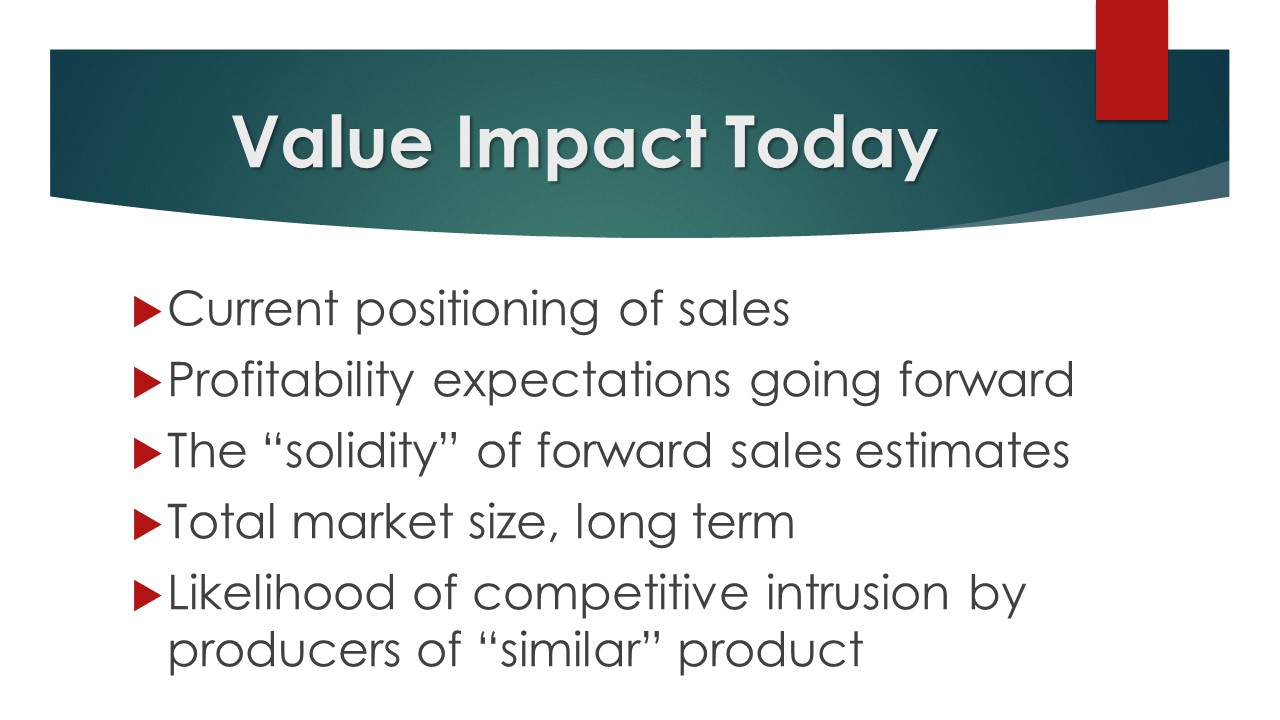

Value Impact Today

So, current positioning of sales, profitability expectations, measurement of those going forward, the solidity of future sales estimates. Do you have good demographic information on where your sales are going to go?

I think of Andy May, and the balance-testing stuff. That’s a great spot! I mean, it really is! You know the demographics are going to increase like crazy. I’m not sure how you protect it. I’m not sure what you can patent or otherwise protect to make it absolutely secure. And, you want to be in front of everybody else. So far, you are, so that’s good. But, I think that will be a beautiful place for a medical device success. It’s going to go well.

A lot of medical device companies have started off tiny. Medtronic was two guys working out of a garage in 1949. Now, they’re $30 billion. That’s amazing. Cook Medical, I just learned they just started in 1953?

Audience member: Six.

Deborah Douglas: Six, I’m sorry. But they’re over $2 billion now. I mean, it’s been a magnificent start from a very early-on time.

The Selling Process

There’s a business author I like. It’s Michael Gerber. He wrote “E Myth.” Some of you probably have read his stuff, way back when. Michael’s a friend of mine, and I like when he talks about his business. He says, “Every business owner wants to sell a business. They all do,” he said, “If they can’t sell a business, they don’t own a business. They own a job!”

There’s truth in that. You really want to create that value. And when the time comes, what I would like to talk about here is just a few little tips about how you go at that when it’s time to sell the company. It’s a tough process, and the competitors are unruly, and it becomes difficult. It’s like a police effort to hold back the competitors. It becomes really rough sometimes.

And finding the right competition is hard. It’s very important, too. We probably spend the first two months doing two things.

The Selling Process: Identifying Buyers

One is figuring out who the competitors are going to be, who’s going to be interested in the company. And, to do that, we talk to a wide array of buyers. We will talk to many different kinds of buyers and we’ll ask them, “What’s your primary target as you make acquisitions today?” We’ll ask them, “What did you buy lately?” We’ll ask them, “What’d you pay for what you bought?”

We can’t always find all of that out, but a lot of it we can. We’ll ask them, “What’s changed in recent times?” What’s new about their direction? That really might make a difference in figuring out which buyers are good for us.

We will talk to an average of probably 300 buyers for one seller to figure out who the right buyers are. After doing all that, we’ll have a list of 30 we think are just right, that we think fit really well. So, it’s worth all of that effort to figure out who those buyers might be and what those buyers might be willing to pay for the company.

And, the best buyers change constantly. Sellers come to us, and, over half the time, they say, “I know who’s going to buy me. It’ll be one of these two or three guys.” They’re always wrong! We’ve done it a long time and they’re always wrong. I mean, it’s never those two or three guys. Maybe the guy who was a great buyer last year has acquisition indigestion. It happens! Maybe there’s new leadership, and that new leadership wants a new direction in the future of the company. Those things make a difference. We try to learn a lot of that, as we talk through this process with the prospective buyers, as we go, and it really helps.

Competition is the key, and we really work hard to make sure competition happens.

We sold a company a few years ago. This was a nice-sized company, about $30 million. Had a really good footprint with its customers, really strong. They all loved him. This company was $30 million in sales, but wasn’t very profitable. They made about $1.5 million on $30 million in sales.

But, we got great competition. And, when the competition got really tough, we ended up selling that company with $1.5 million in profits for $80 million cash. It was amazing! It was a lot of fun [laughs].

And, you can do that if you manage that competition really well. And it’s worth the time.

The Selling Process: Preparing accurate and appropriate data

Now, in that first two months, say, we’re doing that conversation with buyers, but we’re also doing a lot of other things to help to get that information on the company in place. We go through the technical details of the company. We need a lot of information that, typically, we don’t have. Our clients have it.

We get a lot of technical information from our client and put that together really well. We also research a lot of market and demographic information. We tend to be better at that than our clients are. It’s a process of looking hard to see where the market is going, and who’s doing what, and what the future looks like, and what your competitive advantages are in that marketplace. So, it’s worthwhile.

We go through physical inventory of what it’s going to take to manufacture your goods, and we put together a lot of information on that for the buyers. We go through what people skills are needed. What do you have in primary people skills, and what do you need to grow to the next stage? It really helps.

The Selling Process: Competitive Control

We spend our first two months doing those kinds of things, along with the buyer ID, and then we go through the competitive search.

Competition is really key. We sold a company where an owner came to us with a $20 million offer in hand. They said, “We like it. It’s not quite firm yet. But we’re talking to them about $20 million, and we’d like to accept it. But, because they’re not moving very fast, we want you to go ahead and take it and work on getting us other buyers. But, we want you to exempt that buyer from any fees for you.” Well, we said, “We really can’t do that, but, if you like the offer, accept the $20 million offer. Go forward. If it closes, great. If it doesn’t, come back and talk to us, and we’ll help.”

Well, these guys signed a letter of intent that gave them six months. Six months is really long in this business, and we really don’t give anyone more than 60 days, typically. And, the buyer came back to them at the end of six months, and said, “Oh, we don’t quite have our stuff together yet. We need a little more financing. We need a little more due diligence. Can we have 90 days more?” Well, our client said, “Okay,” and gave them 90 days more.

At the end of the 90 days more, they came to us and said, “Okay, we’re ready now.” Well, we started going out to sell the company, put together a package, started talking to buyers, and the original buyer came back to us and said, “Hey, no fair! We’ve done all this work! We’ve spent all this time, and you’re going to sell it without us? It’s just not right!”

Well, in the meantime, we also learned their original $20 million offer had been 80% note, 20% cash. We would never do that! So, we said to the buyer, “Look, you’re welcome to put in a proposal, and we’ll look at it. But, two things. One, we think your price is low. Maybe not crazy-low, but low. And, two, we’re not going to look at any offer that’s not 100% cash at close.”

So, they thought about it for about a week and came back with an offer of $22 million, cash at close, and a $500,000 non-refundable deposit to show their heart was in the right place. It worked! We got it closed. We were fine. Everybody was happy. End of story.

We have another client, right now, actually. This is a client that’s been difficult. They came to us. We did a lot of research on buyers. We were getting started. And, they said, “Well, we only want you to talk to three buyers.” We can’t do that! Three buyers is nuts! It’s really crazy. And, we said, “Okay, we’ll do that at the outset, but then, if we’re not getting it done, you have to open that door for us more.” And, they said, “Okay, we’ll do that.”

Well, the first, their favorite buyer, came to them with an offer of $16 million. That was way low. I mean, this company is not huge and profitable, but they are going to be. I bet they’ll be $300 million in five years. They’re a really good company. So, we told them, “No.” They went away. They came back about four days later and raised it to $20 million. We said, “We’re getting closer, but we’re still not quite there.” Well, they raised it to $25 million, cash at close. Our client was happy and said, “We’re going to take that.”

We were working on the LOI to get the terms worked out before we signed, and one of the other buyers came back and offered us $30 million. We thought that was pretty exciting. Our fees, by the way, are based oddly. They ratchet up. They’re pretty low at a low-end price. Then, we get bonuses, and, in this case, we were in a 10% bonus level. So, they raised it then to $35 million. So, for us, that’s a million. We like that! And our client said, “No, I really like those other guys.”

So, we signed with the other guys. It’s not closed yet, but I think it will. But we want the client to be happy, too. That’s got to be a part of it. And he feels they’re going to be better for his people, better for his product long-term. So, he’s happy, and we’ll get it done.

We sold a pet medical product last year. We’ve done several pet deals over time. This one was small. It was $5 million in sales. Most of our clients are 10-plus. But, $5 million in sales, kind of promising for the future. We ended up with six or eight offers for that company. They were a little under $5 million. We ended up with one that was $12 million, cash at close. We took it! And we closed it! Done! Happy ending! Good place to go.

As you go through this process, it’s worth it to take a little time and effort and to torment over who those buyers might be. It really is a bit of time and effort, but it’s really worth it. And, you can increase your potential so very much by doing that in a short time. There’s a magnificent growth path and potential success.

And, in this industry, it’s also exciting we’re doing things that have healthy innovations that make a difference for people all over the world. So, we like it and we find it exciting. Thank you!

Questions from the Audience

Joe Hage: What strikes me about your line of work, I mean, it’s self-evident, but it’s all about the art of negotiation.

Deborah Douglas: That’s true.

Joe Hage: And, I guess, quantity. You gave an example where they said, “Can you talk to these three people?” And, you’re like, “Uh, I can, but why wouldn’t you expose yourself to everyone who might be interested in you?”

Can you talk about that? Do you end up typically going with one of those three because they have identified it ahead of time?

Deborah Douglas: No, it’s very rare. And we did in this case because our client especially loved the one buyer that came forward with the 16, then the 20, then the 25. They really liked them a lot, and felt that they’d be really great for their people.

They, in the meantime, had become annoyed with the $35 million guy, so it made them not want to take it.

Joe Hage: You talked about, sometimes, coming in too early in the process. Can you help us identify what’s the ideal time to start thinking about it? I believe the unfortunate story is a lot of people begin to think about, “You know, maybe it’s time I begin to get out,” as they’re on the decline.

Can you talk about that?

Deborah Douglas: That is true, and that’s disastrous when that happens. The trend is more important than the numbers, in fact. Actually, the trend is very important.

So, you need to do it while you’re on the climb. Also, most business owners who start and develop that early stage company aren’t the same guys who are going to be great at managing it at a higher level.

So, it’s really prudent to exit before you begin that tail downward. Maybe at the stage where you realize you need to do things you don’t know how to do, it’s time to get help. It’s time to get somebody else in there that can take it to the next stage.

Joe Hage: What’s characteristic of a company that you can’t get the deal done? What are the obstacles to close it? You’re great at what you do, this is your livelihood, you can get a deal done, provided …?

Deborah Douglas: There are very few deals we haven’t been able to get done. We’ve done 130. We’ve failed on four. So, we have a really good track record.

Of the four that we’ve failed, then, one guy had a stroke and was completely incapacitated for months. That was unfortunate. One guy had a 90% customer concentration, and the 90% customer was sold to somebody who owned a competitive division!

Joe Hage: Okay.

Deborah Douglas: Kiss of death.

So, odd things can happen to make it not succeed. But, typically, if you work it very well and you work it very diligently and there’s no huge trauma to the company, we can usually get it done.

Joe Hage: I’m thinking much like a recruiter hiring talent, a company might think, “I could go with them. They’re an expert in what they do. But 35% is a lot. I probably know someone in my network, so let me see if I can fill the job on my own.”

I know about the steep. I recognize that. But I’m wondering, do you find that, in your role, an obstacle for people choosing to adopt someone with your skill set because they’re like, “Well, if I can get $10 on my own, is she really going to get me $13, and I’m just going to lose the $3, so I should just do it by myself and mitigate my risk?”

Deborah Douglas: We find that, if people are looking at professional investment bankers to help them sell, our competition is usually structured the opposite of us. They use a Lehman Formula. 5% on the first $1 million, then 4%, three, two, down to a reclining one.

Ours actually goes the other way. For a typical $10 million seller, we’d be 3% at $10 million, 5% for the 10- to 12-piece, and $10% over 12. So, it’s going in the opposite direction. Usually, most sellers like that because they know we have a strong incentive to get the best deal.

Now, we have occasional guys like our guy right now, who says, “Oh, I don’t care how much it is, I like those guys.” Okay.

Joe Hage: And, sometimes that makes sense.

When you find yourself in that situation, where there’s a pre-determined buyer, is there a role for you or is it like, “Hey, if you know the guy and you’re going to do it, then what do you really need us for?”

Deborah Douglas: Well, you do worry about that, and we think about that. In this case, they really need us because they have a jerk of an attorney who’s made him mad and made him go away three times already [laughs].

Joe Hage: The attorney’s not watching, don’t worry.

Deborah Douglas: So, we can help with that [laughs].

Joe Hage: Okay. Actually, I do have one more. Please indulge me.

Deborah Douglas: Okay.

Joe Hage: If we don’t use Douglas Group or a service like yours, what are the other options for people looking to sell their businesses?

So, what are the array of types of services, and why would they consider going with you versus those competitive options to help you liquidate your position?

Deborah Douglas: I think all of the really viable competitors are going to be full-time sellers of companies. Some of them sell and buy companies. We don’t. We just sell.

You can look at both of those, but all of those are going to be contingent, success-based fees. You really need that because we will have, commonly, hundreds of thousands of dollars into a job. Of course, and you don’t want to have paid us that if we don’t get it finished.

Joe Hage: Fair enough.

Deborah Douglas, thank you very much.

Recent Comments